Australia’s Housing Crisis: How Rising Costs Hurt Wellbeing

How Rising Inflation and Housing Costs Are Undermining Wellbeing in Australia (2026)

1. Introduction

1.1 Hook

A sharp rise in inflation and escalating housing costs is reshaping everyday life across Australia, pushing many families to the brink and intensifying a national affordability crisis.

1.2 Brief Overview

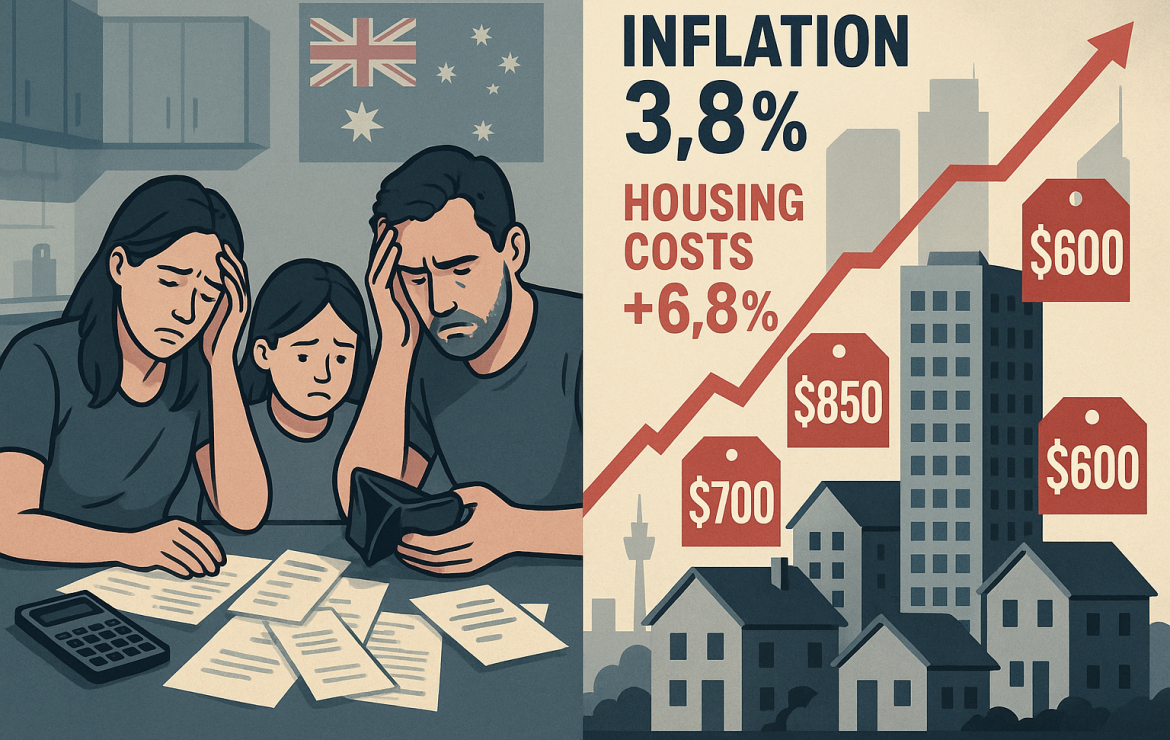

With annual inflation climbing back to 3.8% and housing costs rising by 6.8%, Australian households are facing intensified financial strain. These pressures are eroding mental health, destabilising living arrangements, and widening inequality as more Australians find themselves locked out of secure and affordable housing.

1.3 Thesis Statement

This blog examines how rising inflation and housing costs are undermining wellbeing in Australia. Drawing on current data, expert commentary, and emerging trends, it reveals the depth of the country’s affordability crisis—and what it means for households now and into 2026.

2. Background and Context

2.1 Historical Context

The roots of today’s crisis stretch back decades. Housing transitioned from a basic social need to a speculative asset class in the 1970s, fundamentally reshaping incentives for investors and policymakers. Economist Steve Keen argues that this cultural and political shift laid the foundation for the debt‑driven price inflation we see today.

Fast-forward to the pandemic period: extraordinary stimulus measures and record-low interest rates fuelled a surge in demand. Between 2020 and 2025, home values skyrocketed by 47.3%, adding around $280,000 to the median home price according to Cotality’s housing affordability analysis.

2.2 Recent Developments

Inflation appeared to be easing by mid‑2025, dropping to 2.7% in June. However, the expiry of government energy rebates and global energy market shocks in late 2025 pushed inflation back up to 3.8% by January 2026.

Meanwhile, the RBA’s rate hikes in early 2026—intended to curb inflation—have sharply increased mortgage repayments and contributed to rental increases as landlords pass rising costs on to tenants.

2.3 Current Relevance

Tenants now spend a record 33.4% of their income on rent, and housing stress is worsening across age groups and regions. Homelessness risk is increasing, amplified by the phase‑out of the NRAS program and shortages of social housing.

3. Main Body

3.1 Key Concepts: Inflation, Housing Stress, Wellbeing

Inflation reduces real purchasing power, meaning that even when wages rise, households may still fall behind if essential costs grow faster. Housing stress typically refers to households spending more than 30% of their income on housing—a condition now affecting 71% of Australian households, according to recent findings.

These pressures spill into all facets of wellbeing. Financial strain contributes to anxiety, sleep disturbances, reduced job performance, and even increased family conflict. Stable housing is also foundational for long-term opportunities such as career development, education, and community participation.

3.2 Latest Statistics

Table: Key Australian Housing and Inflation Metrics (2025–2026)

| Metric | Value | Source |

|---|---|---|

| CPI Inflation | 3.8% (Jan 2026) | ABS |

| Trimmed Mean Inflation | 3.4% | ABS |

| Housing Costs | +6.8% | ABS |

| Electricity | +32.2% | ABS |

| New Dwellings | +3.5% | ABS |

| Rents | +3.9% (CPI) | ABS |

| National Rents | +5.5% to Feb 2026 | Cotality |

| Median House Value | 8.9x annual income | Cotality |

| Years to Save Deposit | 11 years | Cotality |

| Households Missing Payments | 32% | Salvation Army |

These data points highlight how sharply costs have surged relative to income growth, deepening financial stress nationwide.

3.3 Expert Opinions

According to Eliza Owen from Cotality, supply constraints, insolvencies, and pandemic stimulus jointly drove unprecedented price rises across the country. Steve Keen offers a contrasting view: it’s not supply shortages but excessive mortgage lending that inflates housing prices. Meanwhile, the RBA points to increased rental inflation due to tight markets, forecasting potential easing only if demand cools. The OECD argues that easing density restrictions is critical to improving affordability.

3.4 Case Study: Perth’s Affordability Collapse

Perth illustrates how quickly affordability can deteriorate under population pressure and supply bottlenecks. Since 2020, Perth’s property values have soared 92%. Population growth hit 17%, but the city delivered only 9% of national new housing completions. Once touted as one of Australia’s most affordable capitals, Perth now faces a median house price 8.9 times the average income.

3.5 Trends and Future Projections

Rents in regional areas are now rising faster than in major cities. Vacancy rates below 2% are becoming the norm. Inner‑city vacant properties and short‑stay holiday homes are further tightening rental markets.

By 2026, unless housing supply expands significantly, cost pressures are expected to continue. Mid-tier capitals like Perth and Brisbane are losing their affordability edge, and more Australians may be pushed into forced relocation or precarious living arrangements.

3.6 Impact Analysis

3.6.1 Societal Impact

Housing affordability stress is now linked to 36% of homelessness cases according to Salvation Army homelessness statistics. Financial pressure contributes to worsening mental health nationwide, with more individuals reporting anxiety, fatigue, and job instability.

3.6.2 Industry Impact

Despite high demand, builder insolvencies are rising due to skyrocketing materials costs and thin margins. Consumer confidence in construction remains low, delaying new projects and further compounding Australia’s supply shortage.

3.7 International Comparison

Table: International Housing Affordability Snapshot (2025–2026)

| Country | Price-to-Income Ratio | Rent as % of Income | Inflation | Notes |

|---|---|---|---|---|

| Australia | 8.9x | 33.4% | 3.8% | Severe supply lag, high debt |

| USA | 5–6x | 28–30% | ~3% | Regional variation |

| Canada | 9–10x (major cities) | 35%+ | 2–3% | Immigration pressure |

| UK | 8–9x (London) | 32% | 2.5% | Long-term supply shortage |

Globally, Australia sits among the least affordable housing markets.

3.8 Controversies and Debates

There remains fierce debate over whether affordability issues stem from supply shortages or excessive lending. “Help-to-buy” schemes face criticism for artificially boosting demand and prices. The gradual phase-out of NRAS is widely seen as contributing to rising homelessness and reduced rental affordability.

4. How to Navigate Rising Costs

4.1 Step-by-Step Actions for Maintaining Wellbeing

- Conduct a personal wellbeing audit by tracking stress levels, sleep patterns, and major spending triggers.

- Reassess living arrangements and consider more affordable alternatives such as co‑living or multigenerational setups.

- Build micro-buffers by setting aside small weekly reserves of $10–$20.

- Create a rent‑proof plan by preparing negotiation strategies and documentation for rent reviews or lease renewals.

4.2 Tips and Best Practices

Form local support networks to reduce grocery and utility costs. Use affordability calculators to assess long-term housing scenarios before making decisions.

4.3 Common Mistakes to Avoid

Avoid taking on new debt during inflation spikes. Don’t rely solely on headline CPI; focus on housing and energy sub-indexes that directly affect household budgets.

4.4 Variations and Alternatives

Remote workers may benefit from exploring regional areas still offering relatively lower rents. Young adults might consider cooperative housing for longer-term stability.

5. FAQ Section

Why is wellbeing affected beyond finances?

Chronic instability undermines sleep, mental health, social connections, and job performance. Financial fear amplifies anxiety, as seen in 2026 wellbeing reports.

How do rising housing costs influence career choices?

Many shift toward gig work or multiple part-time jobs to cope with rising costs, often sacrificing career development.

Are certain demographics more exposed?

Single parents, migrants, and casual workers face higher rent burdens due to fluctuating income and fewer housing options.

Is downsizing always beneficial?

Not always. Lower rents can be offset by higher energy or transport costs in some areas.

Are rent caps effective?

Evidence is mixed. Rent caps provide short-term relief but may reduce new supply unless paired with incentives or increased public housing investment.

6. Challenges and Solutions

6.1 Challenges

Australia faces severe undersupply, escalating construction costs, and shrinking rental affordability. Homelessness rates continue to rise.

6.2 Solutions

Streamlining approvals, expanding public housing, and providing targeted subsidies can help address supply shortages. Reforming debt-driven policies and reinstating affordability programs can reduce speculative inflation.

7. Ethical Considerations and Best Practices

Treating housing as an investment asset rather than a social necessity disproportionately affects younger generations and low-income groups. The removal of programs like NRAS intensifies inequality, raising questions about the ethical responsibilities of policymakers and investors.

Best practices involve balancing investor returns with social wellbeing by prioritising sustainable, equitable housing policies.

8. Success Stories

Victoria offers a blueprint for success. By delivering 33% of national housing completions between 2020 and 2025—despite holding only 24% of the population—Victoria limited home price growth to just 16%, compared to a national 55% surge.

9. Tools and Resources

- RBA inflation trackers

- ABS CPI budgeting tools

- Cotality affordability calculators

- Vacancy monitoring apps tracking <2% market conditions

10. Conclusion

Rising inflation and surging housing costs are deeply affecting wellbeing across Australia. These pressures strain financial stability, mental health, and long-term opportunities. A coordinated approach—combining policy reform, supply expansion, and community-level strategies—is essential to restoring stability and affordability.

11. Additional Resources

Related posts